View:

May 13, 2024

USD flows: USD lifted by higher New York Fed inflation expectauons

May 13, 2024 3:26 PM UTC

The USD has seen a bounce on the New York Fed’s April survey of consumer inflation expectations, showing market sensitivity to the issue. This reinforces a message of stronger inflation expectations in May’s preliminary Michigan CSI report on Friday.

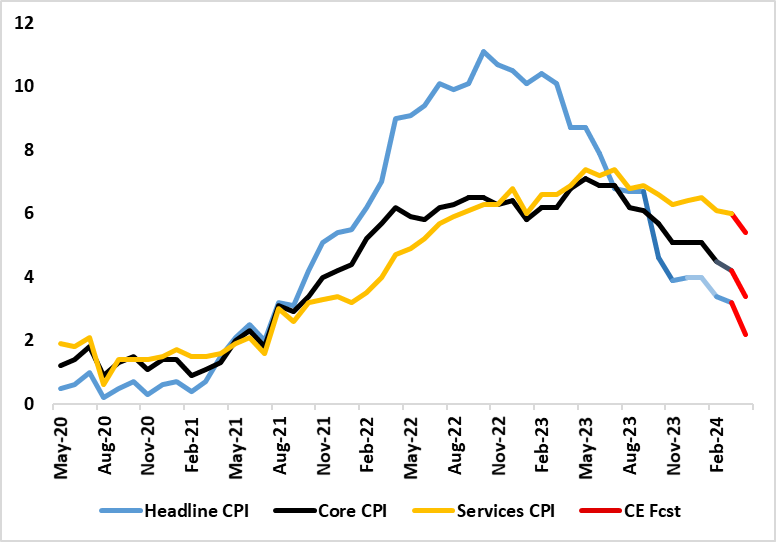

Preview: Due May 14 - U.S. April PPI - New Year strength fading

May 13, 2024 12:26 PM UTC

We expect a 0.3% increase in April’s PPI, with gains of 0.2% in the core rates ex food and energy and ex food, energy and trade. The core rates would match March’s outcome which slowed from above trend gains in January and February.

UK CPI Inflation Preview (May 22): Inflation to Fall Further and More Broadly

May 13, 2024 12:10 PM UTC

It is very clear that labor market and CPI data are crucial to BoE thinking about the timing and even existence if any start to an easing cycle. But perhaps the CPI data is the most crucial making the looming April data all the more important for markets as they weigh the chances of an initial rat

China RRR and Rate Cuts

May 13, 2024 7:54 AM UTC

The latest China money supply and lending figures show that private household and business lending is very subdued. More need to be done to boost credit demand as well as credit supply. However, the authorities desires to avoid too much Yuan weakness will likely mean that the next move is a 25bp

Watts at Stake: India's Looming Power Shortage

May 13, 2024 6:58 AM UTC

India's power sector faces rising demand and power shortages, sparking fears of the most significant power shortfall in a decade. With coal imports continuing to rise and hydropower generation declining, India's aim to become a manufacturing hub could become challenging. Energy transition is likely

USD/JPY flows: BoJ Purchase decrease and Kato's remark Affecting JPY

May 13, 2024 4:37 AM UTC

Japan's Kato says its natural that monetary policy will revert to positive interest rates

Bank of Japan has reduced the amount of 5-10yr JGBs purchased in its latest operation from 475bn JPY to 425bn JPY, comparing to last operation.

Asia Open - Overnight Highlights

May 13, 2024 12:00 AM UTC

EMERGING ASIA

EM currencies perform individually against the USD as the greenback reversed earlier losses on more hawkish market sentiment. THB saw the largest gains of 0.59%, followed by KRW 0.14%, TWD 0.12%, MYR 0.03% and INR & HKD 0.01%; the biggest losers are CNH & SGD 0.16% CNY 0.1% and IDR 0.08