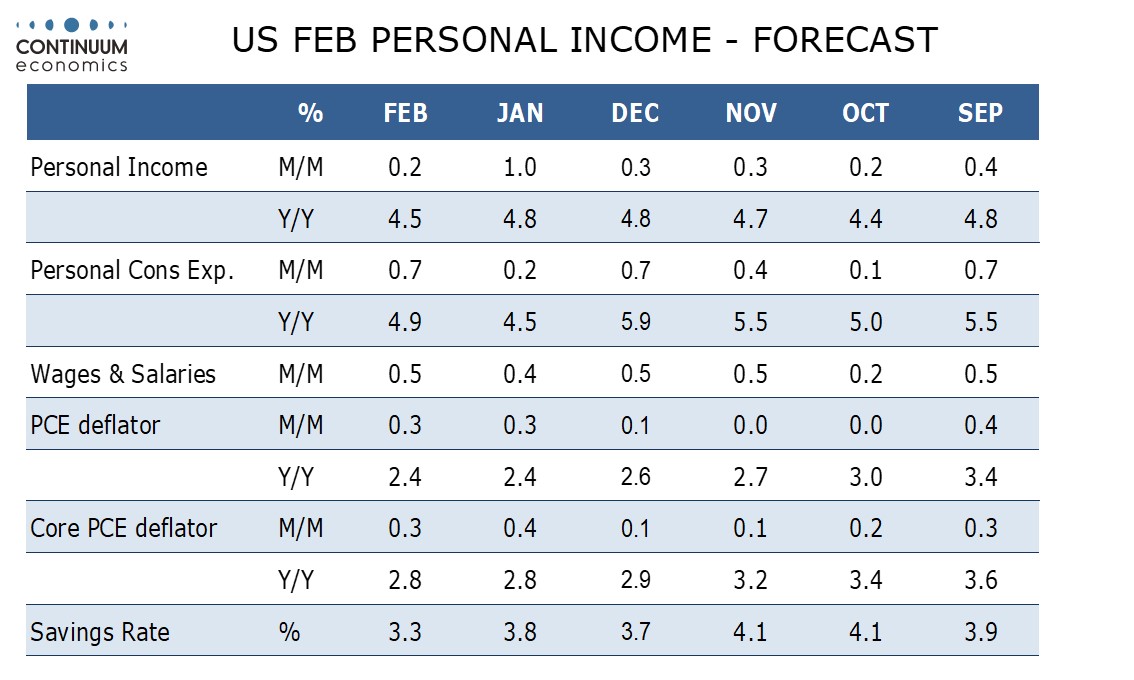

Preview: Due March 29 - U.S. February Personal Income and Spending - Core PCE prices seen less strong than core CPI

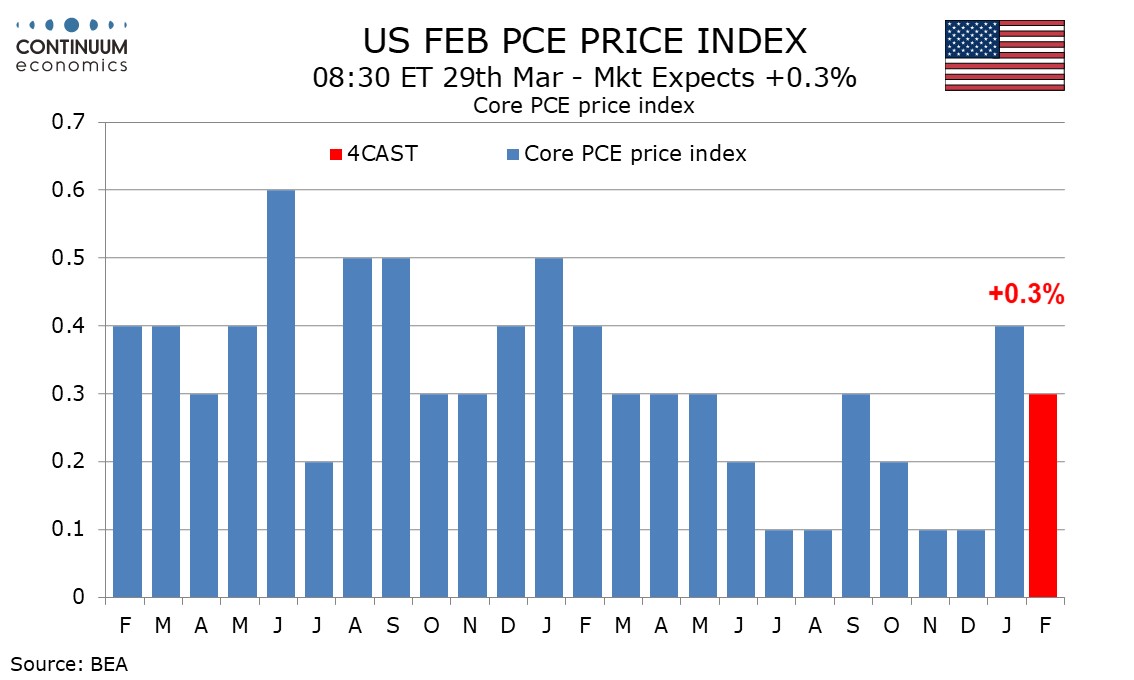

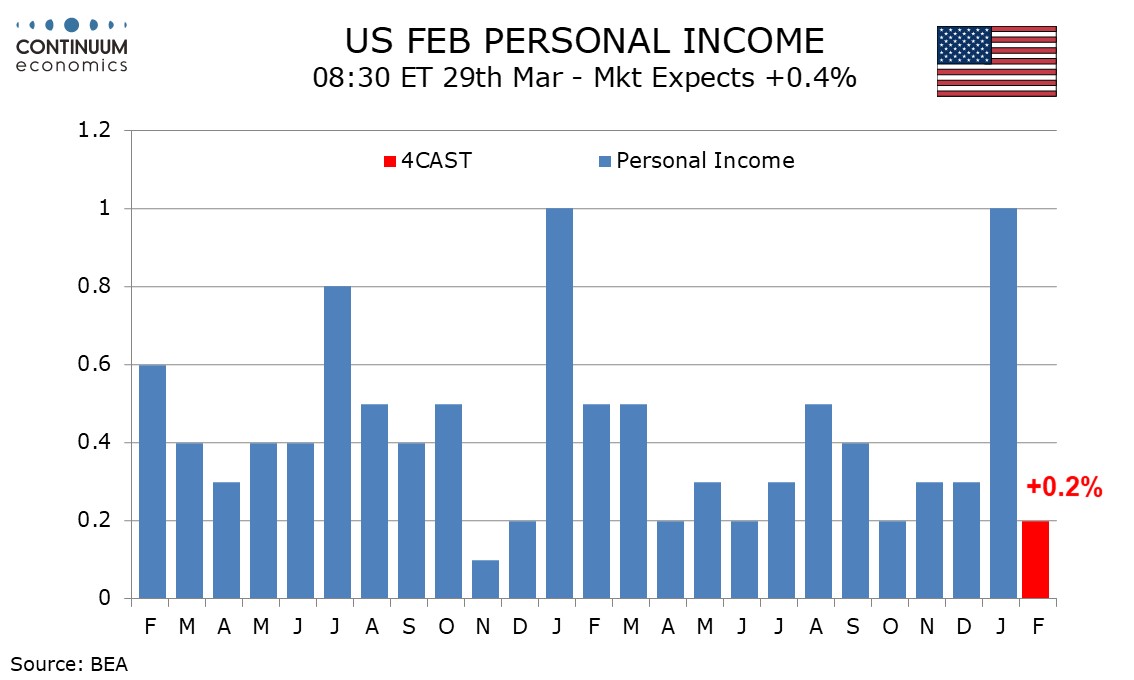

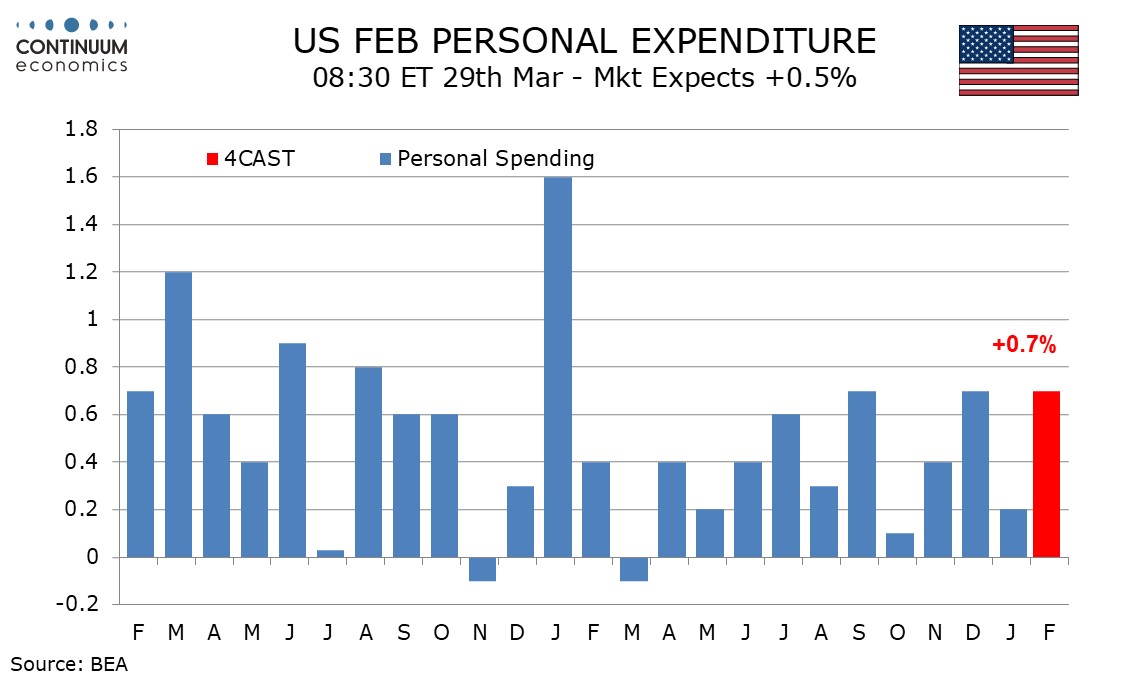

We expect February to deliver a 0.3% increase in the core PCE price index, above most recent months but slower than January’s 0.4% and a 0.4% rise in February’s core CPI, which was up only 0.358% before rounding. We expect a subdued 0.2% gain in personal income to underperform a 0.7% increase in spending.

Core PCE prices usually underperform core CPI, though January was an exception, with both series rising by 0.4% on the month but core PCE prices slightly stronger before rounding. In late 2023 however the core PCE underperformance was sometimes significant, with only one of the seven months to December seeing core PCE prices exceeding 0.2% before rounding. With February’s core CPI rounded up to 0.4%, it is likely that core PCE prices will be rounded to 0.3%. Fed's Powell suggested after the FOMC meeting it may even be below 0.3% before rounding.

We expect overall PCE prices to also rise by 0.3% in February, despite overall CPI being on the firm side of 0.4% before rounding. PCE prices tend to be less sensitive to energy. Yr/yr data would then remain unchanged from January, both overall at 2.4% and ex food and energy at 2.8%.

Strength in non-farm payroll and a rise in the workweek are likely to deliver a healthy 0.5% rise in wages and salaries even with average hourly earnings slowing from January, when wages and salaries rose by 0.4%. We expect overall personal income to underperform wages and salaries rising by only 0.2%, correcting from a strong 1.0% in January. January’s data was lifted by gains in social security, which should persist having come on annual cost of living adjustments, and dividends, which is likely to see correction lower. Disposable income rose by only 0.3% in January as taxes increased. We expect February disposable income to match personal income with a rise of 0.2%.

Retail sales rose by 0.6% in February, not fully reversing a weather-induced decline seen in January, and we expect a similar 0.7% rise in services to bring a 0.7% increase in personal spending. In the case of services, the rise will be slower than that seen in January. Spending outpacing income will see the savings rate fall to 3.3%, its lowest since November 2022, from 3.8% in January. Given that Q4 spending was revised higher, savings may come in even weaker than our forecast.