FX Weekly Strategy: April 1st-5th

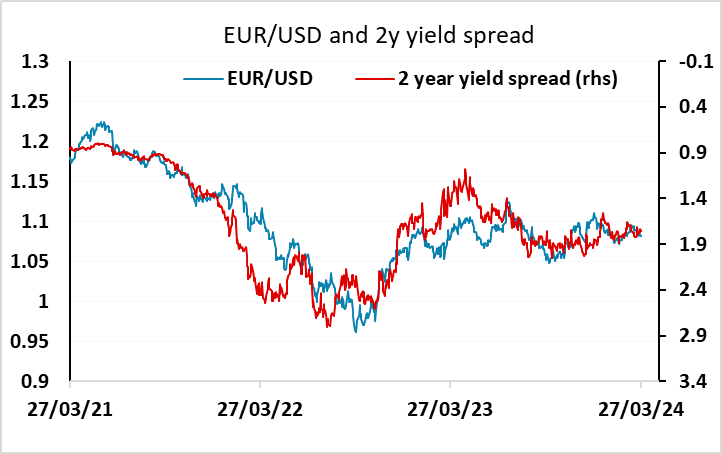

EUR/USD unlikely to break out of the range

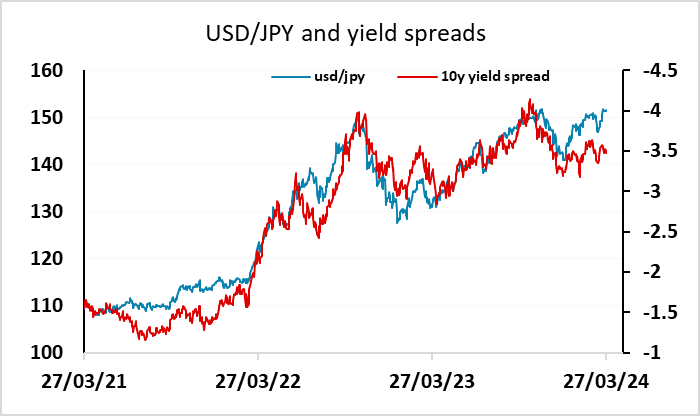

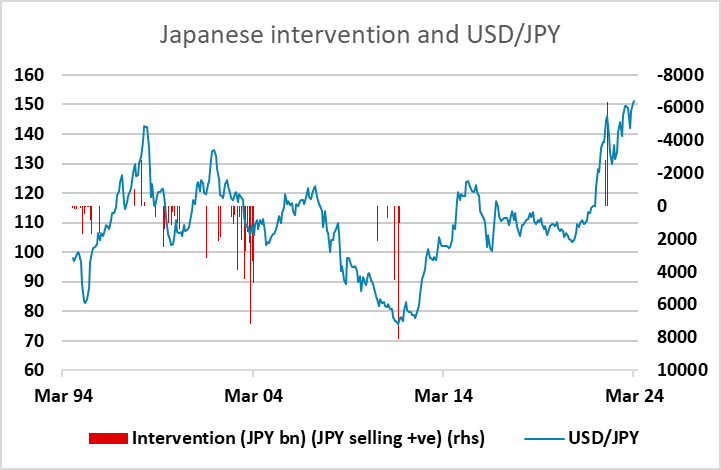

USD/JPY upside looks very limited

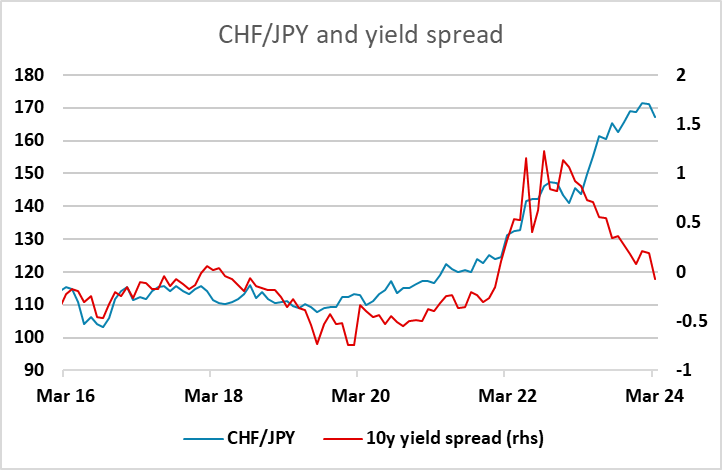

CHF the preferred funding currency

Strategy for the week ahead

EUR/USD unlikely to break out of the range

USD/JPY upside looks very limited

CHF the preferred funding currency

EUR/USD has been stuck in a range through Q1, trading 1.0695-1.1050 with only one visit to each end of the range, and the majority of time spent 1.08-1.09. Part of the problem has been the lack of any significant movement in yield spreads, with rate cut expectations in the US and Eurozone mirroring each other for most of the quarter. To some extent this reflects the fact that inflation has been a global phenomenon in the last couple of years, caused by global supply factors (including the pandemic) rather than idiosyncratic demand factors in individual economies. As it stands, the market prices slightly more easing form the ECB than from the Fed and the BoE this year, but this has fluctuated through Q1. The risk may now be that the Fed reins back its intended easing in the face of relatively strong data, but this will require evidence of more persistent inflation pressures, which they didn’t see as being clear at last week’s FOMC meeting. The US employment report will consequently be the main focus this week, with the average earnings numbers as important as the payrolls, given the focus on earnings growth as a key determinant of service sector inflation. Our forecast don’t suggest any significant deviation from the current trends, and should therefore not be enough to create any expectations of a change in Fed stance.

On the other side of the equation, the Eurozone inflation data is due this week, and we see a further drop in headline inflation to a 31 month low of 2.4%, while we expect core to drop a notch to 3.1%. This will probably not be enough to change market pricing of a 25bp rate cut in June (currently priced as a 95% chance). So it’s hard to see a significant move in front end yield spreads this week. The EUR/USD range is therefore likely to hold a little longer, with the next US inflation data on April 10 and the April 11 ECB meeting probably the calendar items most likely to trigger a significant move.

There has been a lot more volatility in USD/JPY in Q1, and this will remain a major focus coming into Q2. USD/JPY continues to hold close to 34 year highs at 151.97, reached just last week, but is running into repeated verbal intervention from the Japanese authorities, suggesting that any significant gain to new highs could well be met by actual intervention. This is particularly likely if such a move was JPY specific rather than due to general USD strength. There isn’t anything obvious from the Japanese side to move the JPY this week, but the limit on the USD/JPY upside from intervention suggests that there is upside risks for the JPY on the crosses if there is any general USD strength. In any case, USD/JPY continues to trade at levels that look high relative to the yield spread correlation in recent years, so the risks are generally on the JPY upside.

The CHF has been weak in the last few weeks, initially in response to weaker than expected CPI data and subsequently in reaction to the SNB rate cut. There was something of a recovery on Thursday, probably due to end of month/quarter squaring of positions, but this week sees more CPI data which could shape sentiment going forward. While we do still see downside risks for the CHF, this relates more to its high level than the risk of further SNB easing. The SNB’s rate cut may have come before the rest of the G10, but the rest of the G10 are likely to follow in the coming months and are likely to cut more than the SNB in the next year or two (if only because they are starting from higher levels). In any case, the CF does not tend to trade much on yield spreads. The strength of the last year or two has been in part due to relatively low Swiss inflation, which has justified nominal currency appreciation to maintain real values, but also in part due to the SNB unwinding its holding of FX reserves. It has halted this FX selling this year, allowing the CHF to ease. From a value perspective there is more scope for the CHF to decline against the JPY than any of the other currencies. This week’s CPI data could either sustain the recent CHF downtrend or lead to a correction, but the CHF may well have started a longer term decline against the JPY. The CHF now makes more sense as a funding currency given its level, its low rates and the potential involvement of the Japanese authorities to limit the JPY downside while the SNB have stepped away from supporting the CHF.

Data and events for the week ahead

USA

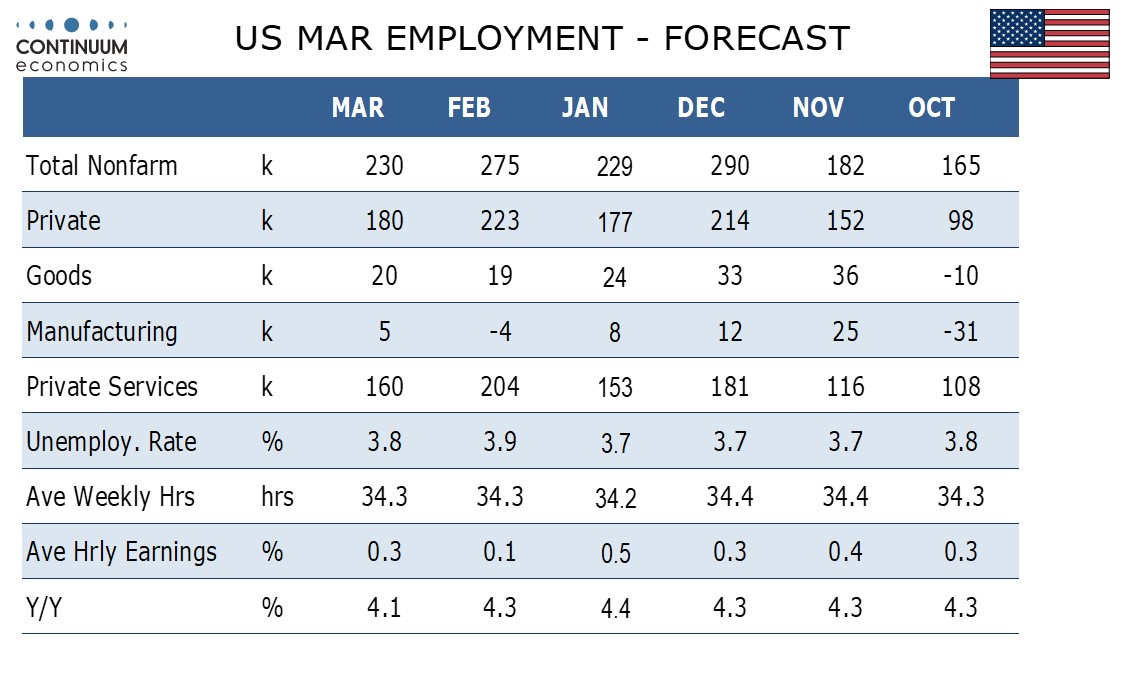

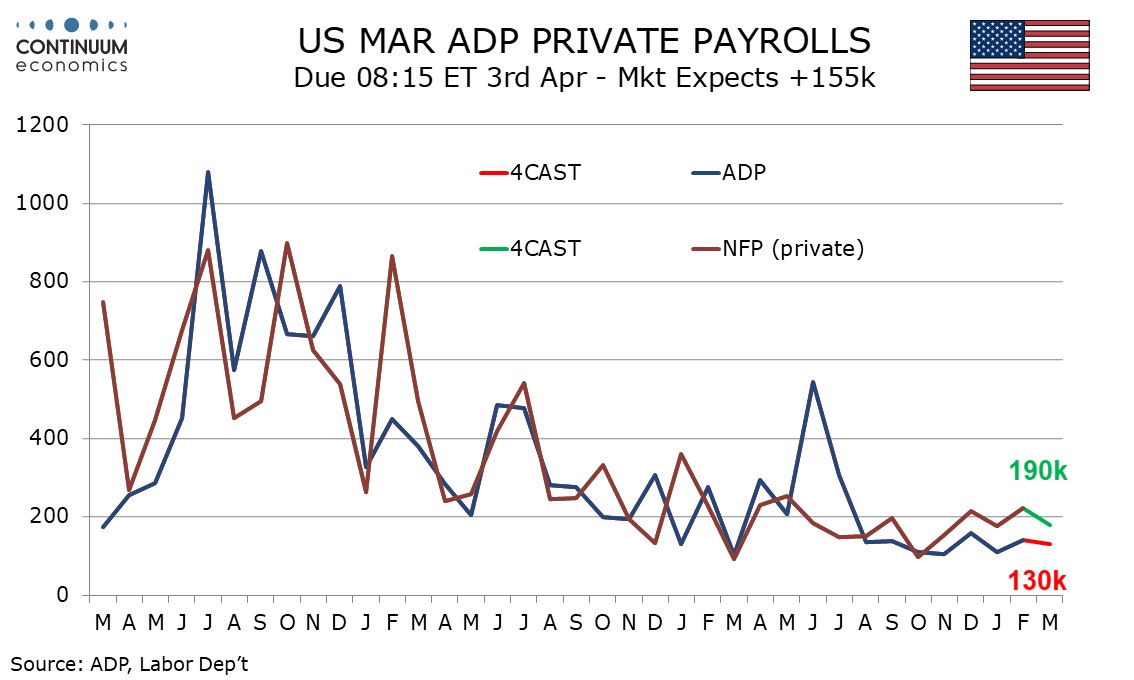

The highlight of the US data calendar is March’s non-farm payroll on Friday. We expect a solid trend to persist with a rise of 230k, 180k in the private sector. We expect a moderate 0.3% rise in average hourly earnings and a correction lower in unemployment to 3.8% from 3.9%. Wednesday we will see March’s ADP estimate for private sector employment growth, where we expect a rise of 130k, in line with recent trend, that has been underperforming the non-farm payroll. Before payrolls Tuesday’s JOLTS report on February labor turnover and Thursday’s initial claims will provide further labor market insight.

On Monday we expect March’s ISM manufacturing index to rise to 49.5 from 47.8 assisted by seasonal adjustments though on Wednesday we expect March’s ISM services index to be almost unchanged at 52.5 from 52.6 in February. The tail end of February data brings construction spending on Monday, factory orders on Tuesday, the trade balance on Thursday and consumer credit on Friday.

Fed speakers will be closely watched, most importantly Powell who speaks on Wednesday. Tuesday sees Williams, Mester and Daly. Scheduled on Thursday are Harker, Goolsbee, Mester and incoming St Louis Fed President Alberto Musalem.

Canada

In Canada, The BoC will be watching its quarterly business outlook survey on Monday closely. March S and P PMIs are due for manufacturing on Monday and services on Wednesday. February’s trade balance is due on Thursday while March employment data, where February data was strong, is due on Friday. Friday also sees March’s Ivey manufacturing PMI.

UK

A holiday shorted week sees an array of survey data with no major revisions expected in the final PMIs (Tue & Thu) but with more sectorial insight coming from the construction PMI (Fri). More interest may be in the BoE decision makers survey (Thu) which has flagged easier cost pressures of late. But perhaps, the data highlight this week is on Tuesday with fresh BoE-compiled money and credit data that may be of increasing importance. Firstly, they will show the extent to which cash-strapped households are still turning to borrowing to fund everyday spending. But secondly, they will highlight how BoE balance sheet reduction is having a wider impact, given the drop in bank deposits that has occurred if late, the question being to what extent is this adding to downward pressure on private sector credit.

Eurozone

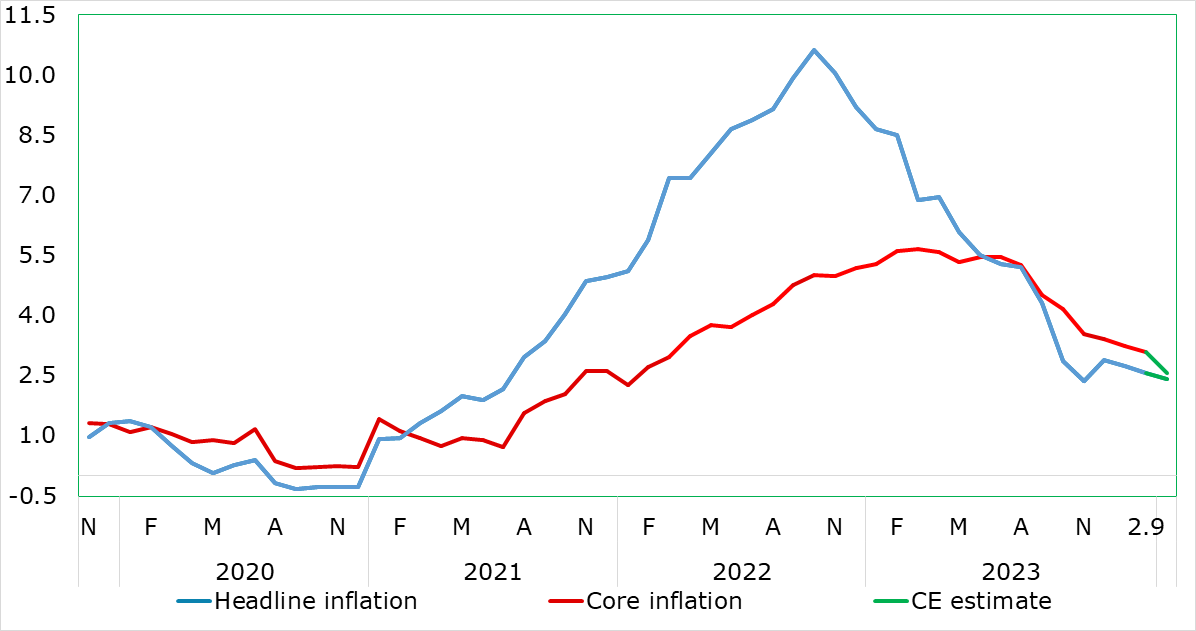

Inflation week beckons with an array of national numbers and the important EZ figure. On Tuesday, in Germany, we see a further and broader fall from 2.7% to a 33-month low of 2.4% in the March HICP data, dominated by a clear fall in food inflation, and a belated drop in services, both possibly held up somewhat by the earlier Easter this year. Wednesday sees the EZ counterpart where we see the headline HICP down to a 31-month low of 2.4%, the latter encompassing more discernibly softer y/y services inflation, in turn pointing to the core rate dropping a notch to 3.1%. It also facing possible Easter-related distortions.

Headline and Core Inflation Falling Further?

Source: Eurostat, CE

Otherwise, PPI data (Thu) may be less soft, while EZ retail sales (Fri) may be directionless still. The main event though is the account of the last ECB Council meeting which will be noted for how broad was the consensus to back the revised inflation projections showing an earlier and sustained drop below target and thus implicitly back market rate pricing. The ECB consumer expectations survey (Tue) may be of declining importance as a result with the final PMIs (Tue & Thu) unlikely to show much revision but with more insight coming from the construction PMI (Fri). Finally, German manufacturing orders data (Fri) may continue to show clear m/m volatility albeit superimposed over weakness.

Rest of Western Europe

There are key events in Sweden, with the minutes to this month’s Riksbank Board meeting providing detail on the much more dovish stance – no formal dissent was evident bu the minutes may show some divisions about the timing and scale of rate cuts envisaged. Switzerland sees what have been hitherto softer-than-expected CPI data (Tue) but where we see a small rise from the 1.2% February outcome.

Japan

Relatively quiet calendar for Japan next week. While Large manufacturing Index on Monday, April 1, is generally more important. We see the overall household spending to be more market moving this time as private consumption data is critical for economic growth forecast. Household spending has been in contraction from the past months on negative real wage and almost dragged Japan into recession.

Australia

RBA meeting minutes and Private Inflation data on Tuesday, April 2, would be on of the key data for Australia, apart from trade balance on Friday, April 5. But very likely neither would be market moving as we do not see such to deviate significant enough to change RBA’s current rate path. We also have some PMI on Wednesday and Thursday.

NZ

We only have building permits on Thursday for NZ.