FX Daily Strategy: APAC, May 10th

GBP unlikely to extend losses on UK GDP

More risk of NOK gains than losses on CPI

CAD may start to underperform on the crosses

USD strength to start to wane

GBP unlikely to extend losses on UK GDP

More risk of NOK gains than losses on CPI

CAD may start to underperform on the crosses

USD strength to start to wane

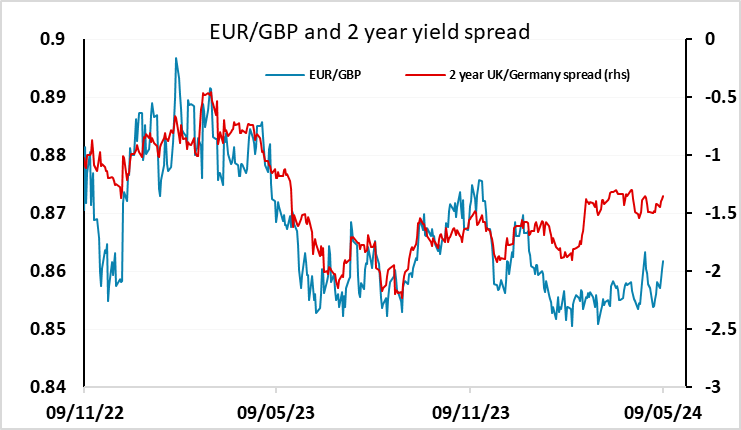

Friday sees UK Q1 GDP, Norwegian April CPI and the Canadian April employment report. The UK Q1 GDP number seems unlikely to surprise as the Bank of England, who may have some inside information, revised up their forecast to be in line with the market consensus at 0.4% in the Monetary Policy Report (MPR) released yesterday. GBP softened a little after the MPR and BoE decision, with the 2 votes in favour of a cut suggesting the possibility that there will be a cut at the June meeting. The market pricing of this was nevertheless not much changed at around a 45% chance, and the decline in the pound was modest. A stronger 0.4% rise in GDP in Q1, even though expected and following a 0.3% decline in Q4, is unlikely to trigger further GBP weakness. This will probably only come if we see evidence of further weakness in wage growth or inflation in the next couple of weeks. For now, although we favour the upside, EUR/GBP probably won’t move far from 0.86.

Norwegian CPI could be of interest given the weakness of the NOK and the relative hawkishness of Norges Bank, who indicated a longer period of unchanged rates was possible at the latest meeting. Core CPI inflation is expected to fall to 4.3% from 4.5% y/y in April, which would be a little below Norges Bank projections. Still, EUR/NOK continues to look extended at current levels. We are only 3% off the 12.06 high from May 2023, which is also the all time high excluding the pandemic spike in April 2020. While the NOK remains a strong currency relative to PPP, it is hard to justify the decline against the EUR by yield spreads or relative economic performance. The risks may therefore be weighted more towards a NOK recovery on stronger than expected CPI than towards a NOK decline on weaker numbers.

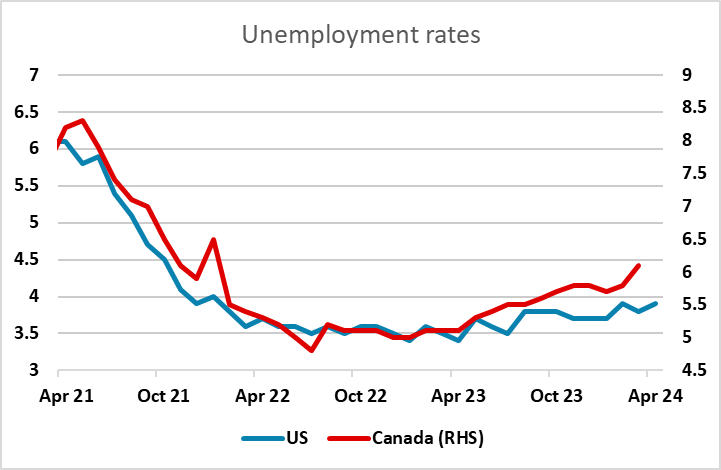

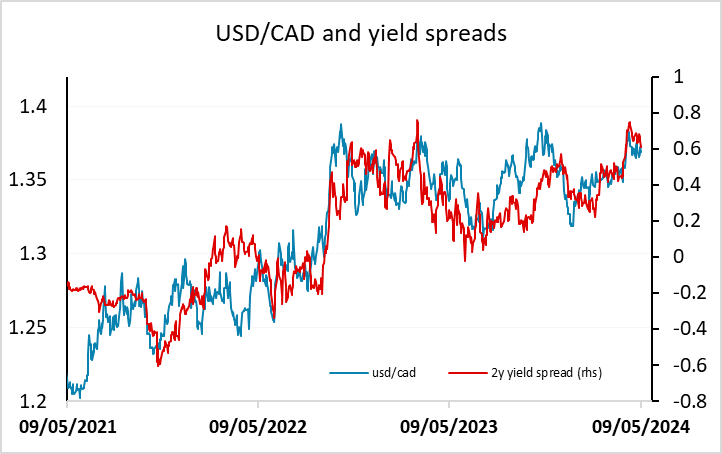

The Canadian employment report is expected to show a modest rise in employment in April after a small decline in March, but the unemployment rate is expected to continue to edge higher to 6.2%. There has been a steady rise in the unemployment rate since mid-2023, which is in contrast to the US performance and suggests we may see some more downward pressure on the CAD. However, this may now be more likely on the crosses than against the USD, following the run of slightly softer US numbers in the last couple of weeks, with the rise in initial jobless claims on Thursday the latest example.

The rise in jobless claims did trigger a softer USD on Thursday, and we are starting to expect a softer USD trend to start to be seen across the board from here which could continue through the rest of this year. It’s early days, but somewhat softer US numbers, somewhat stronger European numbers, BoJ intervention and yield spreads likely to move further in favour of the JPY all suggests we might start to see the USD decline from the high levels it currently holds. It should be remembered that the USD is extremely highly valued by historic standards, particularly against the JPY but also against the EUR, and this is likely to correct in the coming years. Now may be the start.