FX Daily Strategy: N America, May 10th

GBP recovers after UK GDP

NOK edged higher on CPI

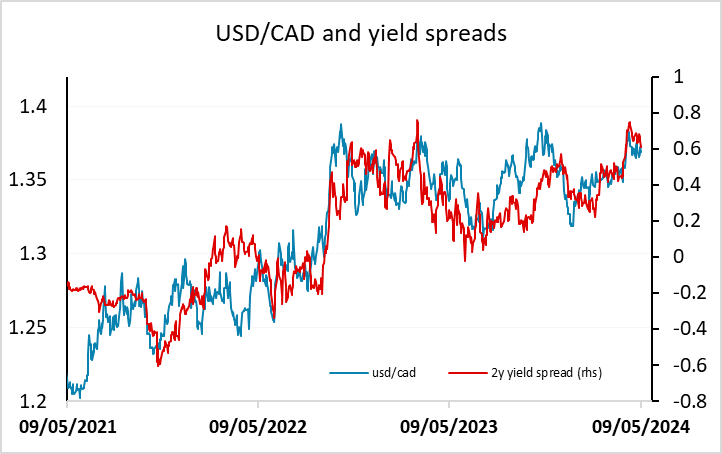

CAD may start to underperform on the crosses

USD strength to start to wane

GBP recovers after UK GDP

NOK edged higher on CPI

CAD may start to underperform on the crosses

USD strength to start to wane

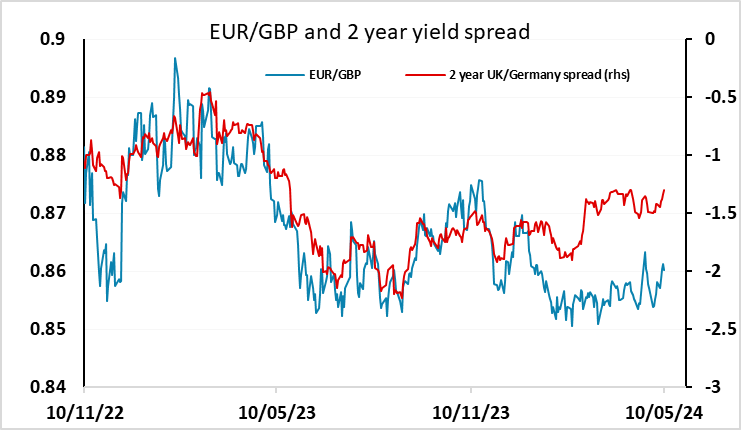

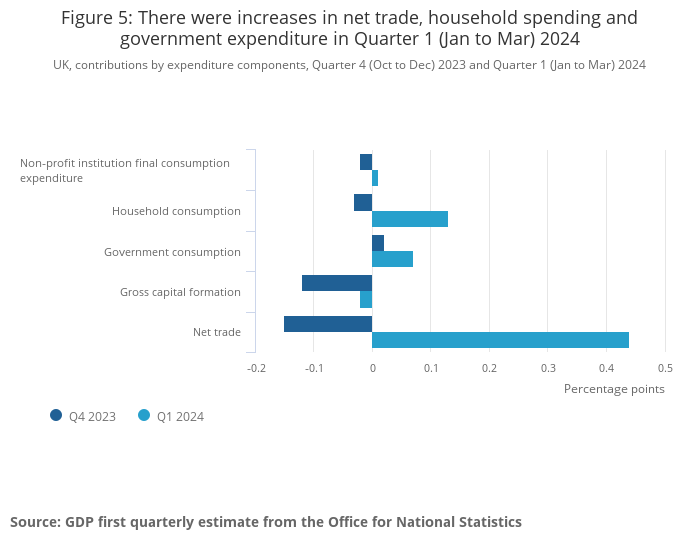

GBP strengthened in early trade, reversing yesterday’s decline after the Bank of England MPC meeting and Monetary Policy Report, driven by stronger than expected Q1 GDP. GDP rose 0.6% q/q, the strongest quarterly rise since Q1 2022, with industrial production and services output both rising strongly, but construction falling again. From the expenditure side, most of the gain was due to strength in net exports, owing to a 2.3% decline in imports. This makes the rise look a little suspicious, as such volatility in net trade is often temporary. However, the output measure is normally the more reliable in the short term, so it may be that the expenditure breakdown changes in the revised data.

For GBP, the focus is still more on the inflation picture which has been less related to growth performance than supply factors in recent years. There is still a prospect of a June rate cut if the April CPI data behaves and there is evidence that wage growth is continuing to ease. So while in the short run today’s data is likely to see some extension of GBP gains with EUR/GBP stretching below 0.86, we still see upside risks medium term.

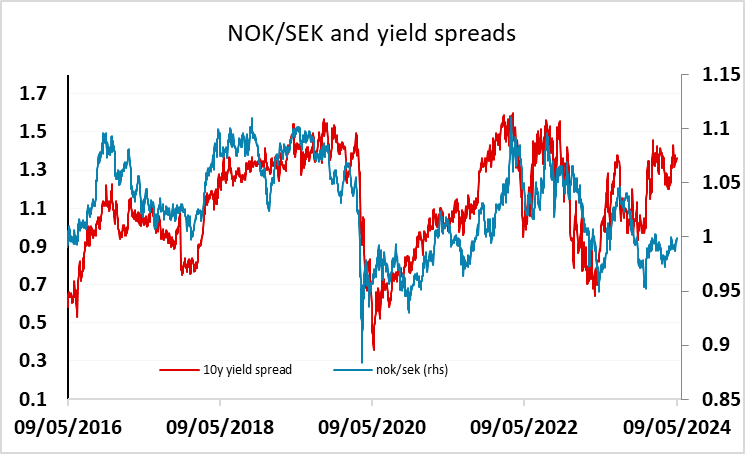

Norway CPI has come in slightly stronger than expected at 4.4% y/y for the core, and the NOK has risen slightly in response, with EUR/NOK down around 2 figures to 11.68. EUR/NOK still looks too high, and NOK/SEK too low, relative yield spreads, and at just around 3% below the all time high just above 12 (excluding the pandemic spike), it is hard to see a rationale for the current NOK weakness.

From a longer term perspective, the NOK has always traded on the strong side relative to PPP, as it typical of currencies of countries with large and persistent current account surpluses, so to that extent even current levels can’t be seen as “cheap”. The NOK weakness may therefore be part of a more general trend for a decline in this historic premium for surplus currencies. If so, there may be scope for the CHF in particular to decline from current high levels. However, with yield spreads still generally the dominant driver of most DM currencies, we still see upside risks for the NOK helped by the relatively hawkish Norges Bank stance.

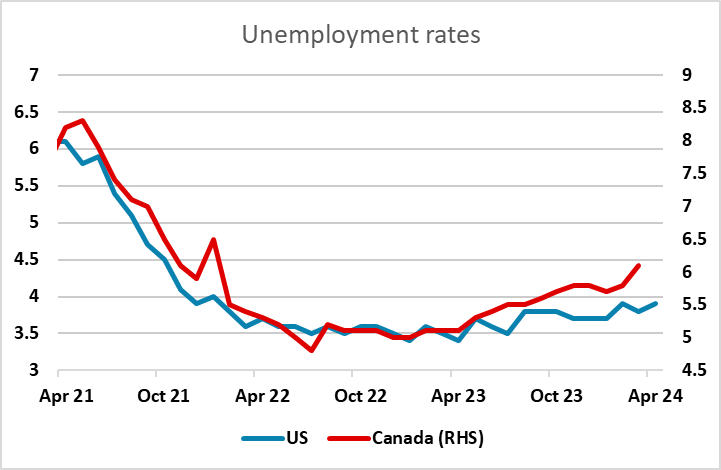

The Canadian employment report is expected to show a modest rise in employment in April after a small decline in March, but the unemployment rate is expected to continue to edge higher to 6.2%. There has been a steady rise in the unemployment rate since mid-2023, which is in contrast to the US performance and suggests we may see some more downward pressure on the CAD. However, this may now be more likely on the crosses than against the USD, following the run of slightly softer US numbers in the last couple of weeks, with the rise in initial jobless claims on Thursday the latest example.

The rise in jobless claims did trigger a softer USD on Thursday, and we are starting to expect a softer USD trend to start to be seen across the board from here which could continue through the rest of this year. It’s early days, but somewhat softer US numbers, somewhat stronger European numbers, BoJ intervention and yield spreads likely to move further in favour of the JPY all suggests we might start to see the USD decline from the high levels it currently holds. It should be remembered that the USD is extremely highly valued by historic standards, particularly against the JPY but also against the EUR, and this is likely to correct in the coming years. Now may be the start.